Presented by Lindsay Olsen – Mortgage Broker, Tweed Coast Home Loans

Subscribe here to receive our monthly newsletter straight to your inbox.

This week saw an Epic Tuesday Afternoon for people who enjoy guessing games, with both the Melbourne Cup and the RBA interest rate announcement happening within an hour of each other – talk about EXCITEMENT!

As it turns out, I guess the RBA decided that their announcement would not be the rate to stops the nation, instead, graciously allowing Knight’s Choice (🐴) to fully enjoy his moment.

In other news, we’ve just added two new suburb profiles to our website. Filled with up-to-date property data, demographics, local amenities, attractions and more – check out the pages for Kingscliff and Banora Point. More to come – stay tuned.

Here’s what we’re covering today:

- This month’s RBA interest rate announcement

- First home buyer perks + current property insights

Let’s jump in!

What just happened with interest rates?

The Reserve Bank of Australia (RBA) has wrapped up its November meeting. Here’s what they’ve decided to do with interest rates:

| OLD RATE | CHANGE | NEW RATE |

| 4.35% | 0.00% | 4.35% |

SURPRISE! The RBA has once again left interest rates on hold at its November meeting. The last time the RBA moved on the cash rate was November last year, so we now have a full 12 months where rates have been stable.

While there’s much chit-chat from the media and economists about when rates might come down, the RBA remains tight lipped on the matter.

Personally, I think it’s a smart move from the RBA to not take part in the guessing game of future rate decisions. It appears as though they’ve learnt their lesson from 2022 when the then Governor stated there wouldn’t be any rate rises before 2024… and then increased rates by 4 percentage points over the next year.

The RBA has instead flagged that the cash rate will need to remain ‘sufficiently restrictive’ (translation: rates won’t change) until they’re confident inflation is moving sustainably towards their target range of 2% to 3%. Over the past year inflation was 3.5% which was significantly lower than the year before, but in the eyes of the RBA, not low enough; and not yet sustainably in the right direction.

So, what do the banks think? The best proxy we have for this is looking at the fixed interest mortgage rates that are on offer at the moment. The trend is that 2-year and 3-year fixed rates are cheaper than 1-year fixed rates and the current variable interest rates right now. This indicates banks (in general) think rates will start to come down within the next 12 months, but fall further (and stay there) over the following 12 to 24 months.

If you’re feeling the pinch of the rising cost of living, why not look at refinancing your biggest debt? If your current home loan interest rate is over 6.50% reach out today so we can discuss your options.

First home buyer perks

Data courtesy of CoreLogic Australia

First home buyers are making up more and more of the value of home loans for owner occupiers.

Up from the 10-year average of 24.8%, first home buyers currently account for 28.6% of the value of owner occupied finance applications.

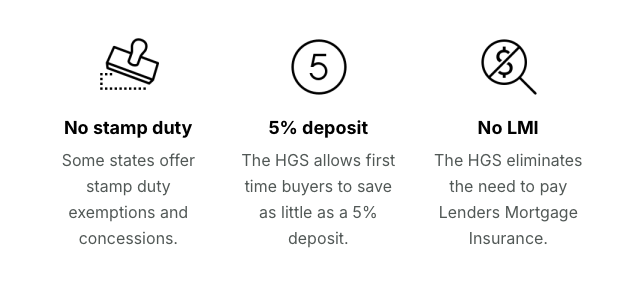

This increase in first home buyers accessing finance can be attributed to government incentives including stamp duty exemptions and concessions, low deposit home loans and elimination of Lenders Mortgage Insurance (LMI). The Federal Government’s Home Guarantee Scheme (HGS) offers 45,000 positions to first home buyers across metro and regional Australia.

We all know that saving a deposit for a house is no small task, particularly if you’re having to pay rent at the same time. The introduction, and continued support, of these government schemes is in my view the best thing to have happened for first home buyers.

If you have any questions about anything in this newsletter, or want to get started on your next property move, please reach out to me directly – I’d love to help you.

Lindsay.