Presented by Lindsay Olsen – Mortgage Broker, Tweed Coast Home Loans

Subscribe here to receive our monthly newsletter straight to your inbox.

The holiday period is always a good excuse to reflect on the past 12 months and plan for the year ahead. What were some of your wins this year? What do you see in your future?

If, like 38% of people, you have a new year’s resolution to improve your finances feel free to get in touch with us to see how we can help. Whether you want to stop renting and start living in your own home; consolidate debt to simplify your finances, refinance your home loan to a cheaper interest rate, or maybe you want to start investing in property – we’re here to guide you through your options and make money easier for you.

Maybe you’re thinking about ways to bring in extra income? If you’ve ever thought about listing your home (or part of it) on Airbnb you won’t want to miss this month’s blog by guest writer, and my favourite person, Alexandra Olsen 👰.

Here’s what we’re covering today:

- New on the blog – Airbnbs as investments

- This month’s RBA interest rate announcement

- Help to Buy scheme is on its way!

Let’s jump in!

New on the blog!

If you’ve ever thought about running an Airbnb – you’ll want to read this post: Airbnb: the good, the bad, and the investment potential.

We share our interviews with 3 Tweed Coast Airbnb hosts, all about their personal experiences setting up and running Airbnbs. We then overview the pros and cons of short-term rentals, and finally, answer the question everyone wants to know – how much money can you make through Airbnb, compared to traditional, long-term rentals?

What just happened with interest rates?

The Reserve Bank of Australia (RBA) has wrapped up its December meeting. Here’s what they’ve decided to do with interest rates:

| OLD RATE | CHANGE | NEW RATE |

| 4.35% | 0.00% | 4.35% |

The RBA is trying their best to stay on Santa’s ‘Nice’ list by keeping rates on hold for another month. I’m sure they could have sealed the deal with a December rate cut, but given that they haven’t increased rates all year I think they’ll still find something under their Christmas tree from the man in red this year.

So with all the Santa puns exhausted…

In keeping with their recent talking points, the RBA has reiterated the three pillars supporting their decision to keep rates on hold:

- Underlying inflation remains too high

- The outlook remains uncertain

- Sustainably returning inflation to target is the priority

At 3.5%, inflation is is still sitting higher than the RBA’s target range of 2% to 3%. Whilst it has come down significantly from its heights of 6.8% in December of 2022, the rate at which inflation is falling is of concern to the RBA.

The most recent RBA forecasts don’t see inflation maintaining consistency at the midpoint of the target range (i.e. inflation at 2.5%) until 2026. However, as additional data rolls in the RBA is gaining confidence that inflation is starting to move sustainably towards the target range, and this is a good thing for anyone with, or about to get, a mortgage.

So, what do the banks think? The best proxy we have for this is looking at the fixed interest mortgage rates that are on offer at the moment. The trend is that 2-year and 3-year fixed rates are cheaper than 1-year fixed rates and the current variable interest rates right now.

This indicates banks (in general) think rates will start to come down within the next 12 months, but fall further (and stay there) over the following 12 to 24 months.

If you’re feeling the pinch of the rising cost of living, why not look at refinancing your biggest debt? If your current home loan interest rate is over 6.50% reach out today so we can discuss your options.

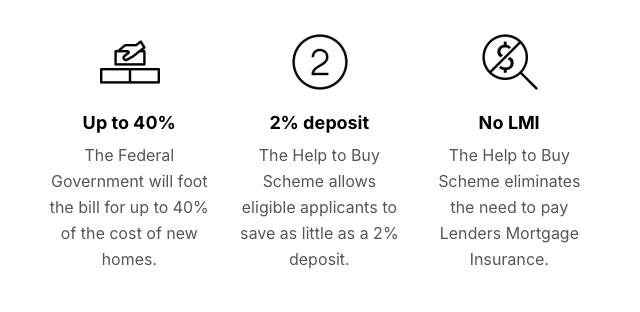

Help to Buy scheme is coming!

Helping low and middle income earners get onto the property ladder

One of the key housing policies promised at the 2022 Federal election has recently been passed into law by parliament. But what is the Help to Buy scheme?

The Help to Buy scheme will allow eligible applicants to co-purchase a home with the Government.

The Federal Government will give buyers the chance to accept an ‘equity contribution’ of 30% for existing homes and 40% for new homes.

But what does this actually mean? It means that the Government will own 30% to 40% of your house’s value. You will need to take out a mortgage to cover the remaining cost of the house (less your deposit). When you sell, you need to pay the Government back for their initial 30% or 40% stake as well as the same proportion of the capital growth.

Eligibility criteria will apply, with a key detail being income and property price caps.

Edit: As of 22 March 2025, income caps have changed. You’ll now need a yearly income of less than $100,000 if buying individually (raised from $)90k) or $160,000 if buying with someone else or as a single parent (raised from $120k). Property price caps vary based on location, and will be linked to average house prices in each area.

Unlike other housing incentives, the Help to Buy scheme is NOT limited to first home buyers; however, you can’t own any other land or property if you’re going to participate in the scheme.

If this is of interest to you, please reply to this email and we can walk through the detail with your personal situation in mind.

If you have any questions about anything in this newsletter, or want to get started on your next property move, please reach out to me directly – I’d love to help you.

Lindsay.