Presented by Lindsay Olsen – Mortgage Broker, Tweed Coast Home Loans

Subscribe here to receive our monthly newsletter straight to your inbox.

A lot has been happening in the world of home loans and property since our last update and this newsletter is full of good news! 🥳

Here’s what we’re covering today:

- Good news for borrowers with study/training debt

- This month’s RBA interest rate announcement

- National property update

Let’s jump in!

Good news for borrowers with study/training debt

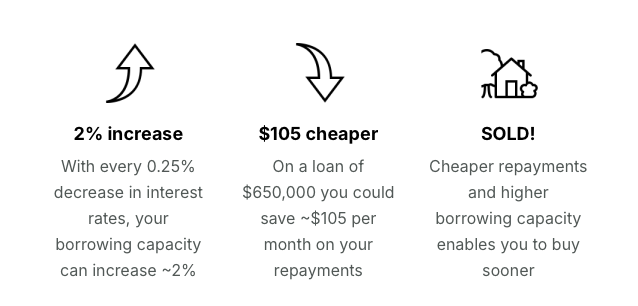

Currently, lenders are required to include HECS/HELP and other study/training loans when assessing a potential borrower’s debt exposure. This is most apparent in the Debt-to-Income Ratio (DTI). Many banks will restrict the borrowing potential of customers to, say, a DTI of 6. Meaning, if you earn $100,000 per year the maximum amount of debt you should be able to access is 6 times this amount, or $600,000.

When lenders are currently assessing the DTI of borrowers with HELP debts, the outstanding balance is included within the maximum debt allowance of the debt-to-income ratio.

Using the same example from above, with a maximum DTI of 6, if you were earning $100,000 per year but had a $20,000 HELP debt, the most you could borrow for a home loan would be $580,000.

The Federal Treasurer, Jim Chalmers, says this new directive will ‘make it easier for Australians with a HELP debt to responsibly take out a mortgage and buy a home’.

The precise details, eligibility criteria and implementation dates of this new approach remain unannounced as yet, but on the face of it I can see this tweak may lead to guidelines that will assist more people into the housing market – which is always a good thing!

Interest rates drop 0.25%

The Reserve Bank of Australia (RBA) has wrapped up its February 2025 meeting. Here’s what they’ve decided to do with interest rates:

| OLD RATE | CHANGE | NEW RATE |

| 4.35% | -0.25% | 4.10% |

FINALLY – the RBA has this week REDUCED interest rates for the first time since November 2020.

The main factor behind this change is that inflation has fallen substantially since its peak in 2022. The most recent data shows inflation for the December quarter at 3.2% which is within touching distance of the RBA’s target range of 2% to 3%. The supporting notes from the RBA announcement even suggest that inflation pressures are decreasing faster than originally anticipated.

While this rate cut is a move in the right direction, I’m not counting on another cut at the next RBA announcement. When you consider the conservatism of the RBA and their goal for inflation to continue decreasing towards their target of 2.5%, it’s no surprise that they flag the following cautions about future rate decisions:

- The Board’s assessment is that monetary policy has been restrictive and will remain so after this reduction in the cash rate

- The Board remains cautious on prospects for further policy easing

- If monetary policy is eased too much too soon, ‘disinflation’ (their word, not mine) could stall, and inflation would settle above the midpoint of the target range.

How have banks reacted to interest rate cuts?

Pleasingly, within minutes of Tuesday’s RBA rate decrease announcement I had received confirmation that banks were starting to pass on the rate cut IN FULL.

Now, this isn’t something that will take effect immediately. The earliest effective date I’ve seen so far is February 27th (:ubank) and the latest so far is March 17th (Thinktank).

If you haven’t heard anything from your bank by the time you read this newsletter, I have all my fingers and toes crossed that most, if not all, lenders will be decreasing their variable interest rates by 0.25%. 🤞

If you’re feeling the pinch of the rising cost of living, why not look at refinancing your biggest debt? If your current home loan interest rate is over 6.50% reach out today so we can discuss your options.

What do interest rate cuts mean for you?

Whether you’re in the market for a home loan, have recently bought your first house, or you have an investment portfolio with multiple loans; all you really want to know is, ‘what does a rate cut mean for me?’.

If you have any questions about anything in this newsletter, or want to get started on your next property move, please reach out to me directly – I’d love to help you.

Lindsay.