If you’re a property owner or thinking of buying in the future, changes are you’ll have a vested interest in how the upcoming election will affect the housing market.

In today’s blog, we’ll summarise what you might want to know ahead of the election.

Here’s what we’re covering today:

- Election promises – which parties offer the best housing support?

- This month’s RBA interest rate announcement

- National property update

Let’s jump in!

How the election will affect the housing market

Australians will go to the polls on May 3 this year to elect the next Federal Government. Front of mind for many voters (sausage aside) will be housing policy, and which party could potentially offer them the best support when it comes to buying a home, or securing a rental.

I thought it’d be a good opportunity to bring together the key housing policies that have been announced by the 3 largest political parties in the country, namely Labor (ALP), the Liberal-National Coalition (LNP), and the Greens.

This isn’t a ‘how to vote’ card, and I’m certainly not trying to push any agenda – this is simply information that I hope you find useful.

Labor

- Help to Buy Scheme: a shared equity scheme where the Government would own up to 40% of your home, reducing the size of your required mortgage

- Building 1.2 million homes: $33 billion over 10 years to the ‘Homes for Australia Plan‘

- Remove red tape: provide $120 million to incentivise States to remove red tape and help more homes be built faster

- 2-year ban: foreign investors wouldn’t be allowed to purchase existing homes for 2 years.

Coalition

- Access to superannuation: first home buyers could access up to $50,000 from their super to buy a home (it needs to be returned to Super when the home is sold)

- Unlock up to 500,000 new homes: invest $5 billion to fund essential infrastructure at new housing development sites

- Freeze red tape: freeze any further changes to the National Construction Code for 10 years

- 2-year ban: foreign investors and temporary residents wouldn’t be allowed to purchase existing homes for 2 years.

Greens

- Stop unlimited rent increases: limit increases to 2% every 2 years

- Phase out tax breaks: for investors with more than 1 investment property, reduce/phase out negative gearing and the capital gains tax discount

- Bring down mortgages: regulate the banks in order to reduce mortgages

- Build public and affordable homes: a Government-owned developer to build quality homes sold and rented at affordable prices.

Now, some of these policies might sound great, some might not, and others might sound like they’re lacking in detail. And that is ultimately the case for the moment. There isn’t a great amount of substance on any of the 3 parties’ websites about how their housing policies might work, or even how realistic they are, so take them with a grain of salt and don’t blame me if they don’t come to fruition 😬.

We can never be certain how an election will affect the housing market – but it always pays to do some research before you hit the polls.

Government raises the income bar for the ‘Help to Buy’ scheme

In a recent blog, we reported on the government’s Help to Buy scheme, and now we’re happy to update that as of March 22, 2025, there have been some changes to income caps:

To summarise: The Help to Buy scheme will help people buy property sooner. The Federal Government will give buyers the chance to accept an ‘equity contribution’ of 30% for existing homes and 40% for new homes.

You’ll need to take out a mortgage to cover the remaining cost of the house (less your deposit). When you sell, you need to pay the Government back for their initial stake as well as the same proportion of the capital growth.

Following last week’s changes, you can now earn a yearly income of less than $100,000 if buying individually (increased from $90k) or $160,000 for joint buyers or single parents (increased from $120k).

Property price caps will apply, and will vary based on location.

The scheme is expected to open for applications later in 2025.

What just happened with interest rates?

The Reserve Bank of Australia (RBA) has wrapped up its April meeting. Here’s what they’ve decided to do with interest rates:

| 4.10% | 0.00% | 4.10% |

| OLD RATE | TUESDAY’S CHANGE | CURRENT RATE |

Not a huge surprise this one, given that the previous decision to drop interest rates was the first rate drop in over 4 years.

I sense the RBA will remain cautious when lowering rates so as not to inadvertently undo the hard work that Australians have done collectively over the past few years in helping to tame inflation.

Inflation is heading in the right direction (i.e. down) for the moment, and, remarkably, it’s within the RBA’s desired band of 2% to 3%; it sits at 2.7% as of the latest monthly data.

Once the RBA believes inflation is under control, it’s likely to further reduce interest rates. My read on the situation is that the RBA will want to see a bit more evidence of inflation holding within their target band for a bit longer, as well as waiting to see the impacts of the United States’ announced tariffs, before making another cut to rates.

If you’re feeling the pinch of the rising cost of living, why not look at refinancing your biggest debt? If your current home loan interest rate is over 6.25% reach out today so we can discuss your options.

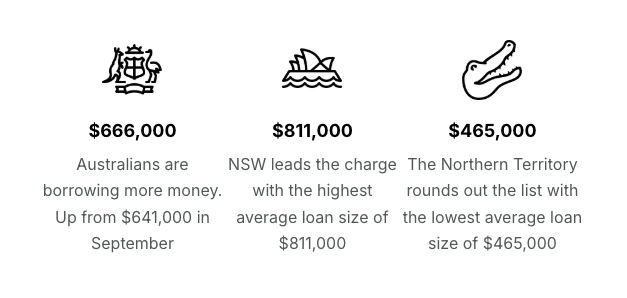

Latest property stats: average home loan size increases

Despite a drop in new home loan approvals, mortgage sizes are climbing.

The most recent Australian Bureau of Statistics data shows the number of home loans declined by 0.4% quarter-to-quarter in December. Despite this, the total value of loans increased 1.4%.

If you have any questions about anything in this newsletter, or want to get started on your next property move, please reach out to me directly – I’d love to help you.