Interest rates have just bumped up by 0.25% following the RBA’s first meeting for 2026. Today we’re answering your questions about refinancing your home loan in the wake of the interest rate rise and the potential for future increases.

Let’s take a look at what’s happening, and what it means for you. Here’s what we’re covering:

- The latest RBA announcement

- How will your repayments change?

- Should you refinance?

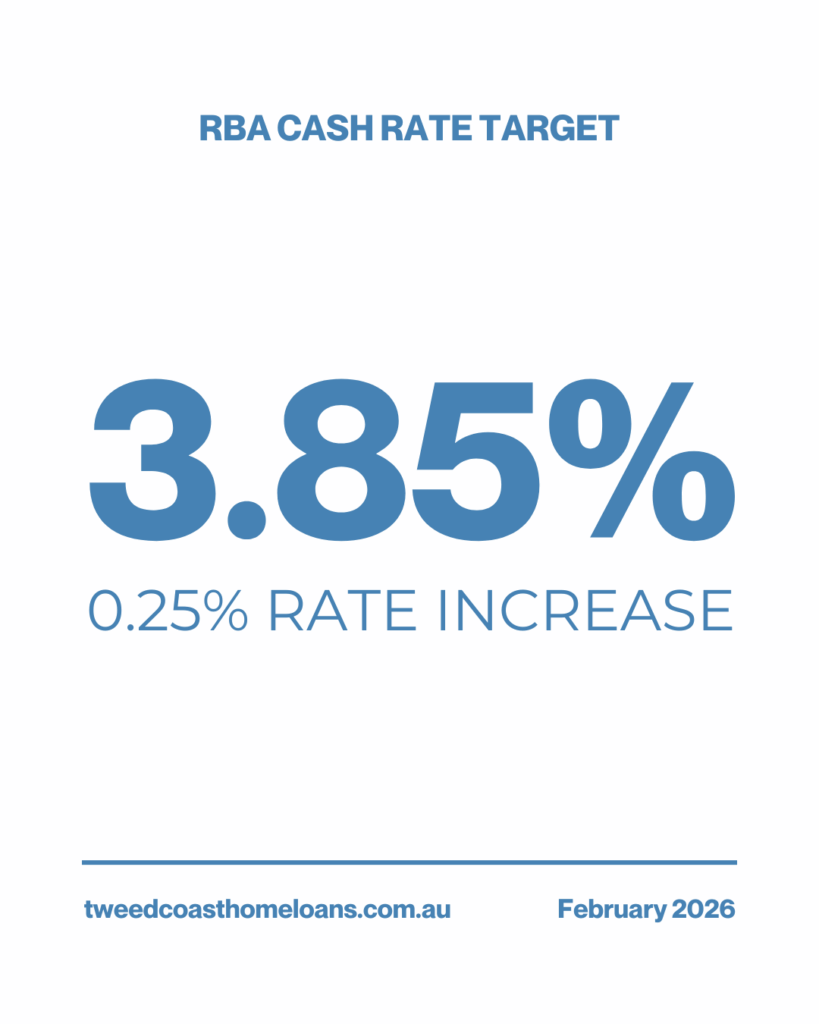

Reserve Bank of Australia raises cash rate to combat inflation

On Tuesday 3 February 2026 the Reserve Bank of Australia lifted the cash rate by 25 basis points to 3.85%.

This is the first upwards move for interest rates since November 2023.

Home owners will of course be disappointed by this news, as interest repayments naturally rise with increases to interest rates.

Prospective home buyers could feel doubly disappointed as this rise will also see their borrowing capacity reduced.

| OLD RATE | CHANGE | NEW RATE |

| 3.6% | 0.25% | 3.85% |

If you’ve been receiving our property updates for some time, you’ll know that inflation is one of the key metrics that influences the RBA’s decision making on interest rates. This month is no different. With the latest data showing inflation for the 12 months to December rising 0.4% to 3.8%, many felt the RBA had no choice but to lift rates in an effort to combat inflation getting too far away from their desired ‘sweet-spot’. The RBA are more comfortable when inflation sits between 2% and 3%.

In justifying their decision, the RBA finished their announcement by flagging that inflation is ‘likely to remain above target for some time’. In our eyes this could potentially point to further rate rises through 2026.

How will increased interest rates affect your home loan repayments?

What does a 0.25% interest rate rise actually mean for Aussie families and their monthly mortgage repayments?

Here’s a quick reference guide to help you understand how much more you might pay:

| Loan amount | Old payment | New payment | Monthly +$ |

| $1,000,000 | $5,678 | $5,836 | $158 |

| $900,000 | $5,110 | $5,252 | $142 |

| $800,000 | $4,542 | $4,669 | $126 |

| $700,000 | $3,975 | $4,085 | $110 |

| $600,000 | $3,407 | $3,501 | $95 |

Note: Assumes a current interest rate of 5.5%, a 0.25% increase in February, a 30‑year loan term with monthly principal and interest repayments, all figures rounded to the nearest dollar.

Is this good time to refinance your home loan?

Just because interest rates are changing doesn’t mean you need to refinance your home loan. What’s more important is if your home loan, and its interest rate, are still serving you in the best way possible.

If you’ve had your home loan for more than a few years it is always worth checking to make sure that you’re still getting a good deal. Because if you’re due for a refinance, you could end up reducing your monthly repayments (and you’re less likely to feel the impact of this latest interest rate rise).

Banks offer their best interest rates to new customers and then as time goes on (particularly as rates drop) existing customers don’t receive the same sharp rates (and if you’re not on the books with a good mortgage broker, rest assured your bank is NOT going to call you out of the blue to ask if you want to give them less money 😂).

Outside of interest rates, a lot of life happens in a few years, too. When you signed up to your current loan it was based on your circumstances back then. By now you might have earned a pay rise, you might have paid down extra off your loan, maybe your low fixed interest rate has ended, or you might be in a position to consider buying an investment property with your home equity.

If your interest rate is no longer competitive, yes, absolutely you should be refinancing. Outside of that, it’s those larger life changes that typically warrant refinancing.

So, no, interest rate rises aren’t the reason to refinance, but they’re a good reminder that you might want to look into it, anyway.

Think you’re due to refinance? We’re ready to help you. Give us a call, email or text – we’d love to chat and see what we can do.